8 Steps to Property Investment Success

There has been lots of hype in the media recently about property investment and the property market, which has left many potential property investors confused about whether or not they should invest.

Like many investment strategies, property investment can be a risky business so it’s important to understand the fundamentals before risking your life savings to ensure that you achieve your financial goals.

When it comes to property investment, there are some important elements to consider, which can be the difference between making or losing money.

In this article, we explain eight key drivers that contribute towards successful property investment.

1. Location, Location, Location

The most important element of all when investing in property is the location. It should come as no surprise that it is actually the land that is the main driver of property growth, not the house itself.

As a general rule of thumb, approximately 80% of capital growth is driven by the land and only 20% by the house, which emphasises the importance of buying the right land in the right location.

Many investors fall into the trap of falling in love with properties in locations that don’t make investor grade and as a result, their return on investment is not optimised.

Generally speaking, an average house in a great location is better than a great house in an average location from an investment perspective. However, choose carefully as the wrong house could undo all the good work you have done in selecting the right location.

Identifying and purchasing properties in suburbs that are in, or are about to go through the gentrification process can also be highly lucrative, as significant increases in capital growth generally occur when this happens.

When selecting a property to purchase, it is recommended that the property is located in close proximity to the following in order to optimise capital gains and minimise vacancy rates:

- Employment

- Infrastructure

- Public transport (trams, trains, buses)

- Schools

- Hospitals

- Shops

- Cafes

- Restaurants

- Parks and recreational areas

Areas to avoid include:

- Properties situated on main roads or in close proximity to unsightly locations and landmarks.

- High crime rate suburbs.

- Areas with lots of vacant land lots (this means that there is plenty of supply, which can negatively affect property prices).

- Single industry towns and locations with only a small number of industrial sectors. The reason being that if a factory or mine closes down, house prices can fall dramatically.

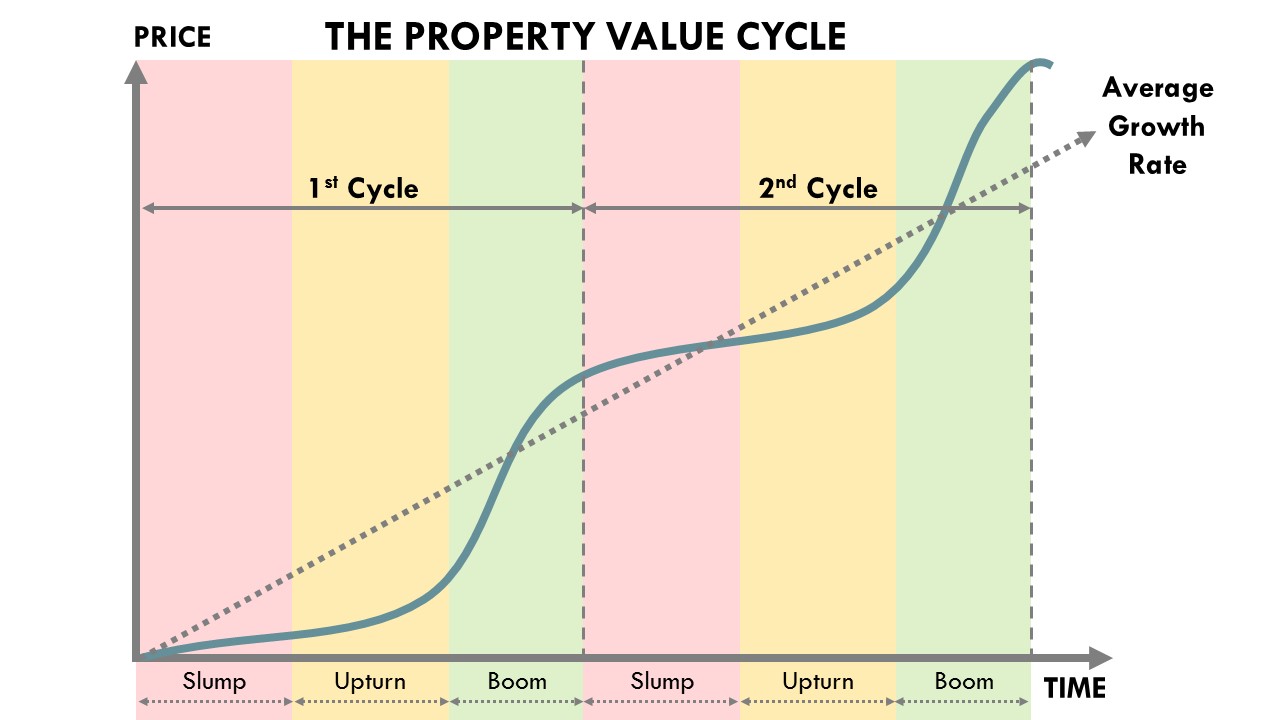

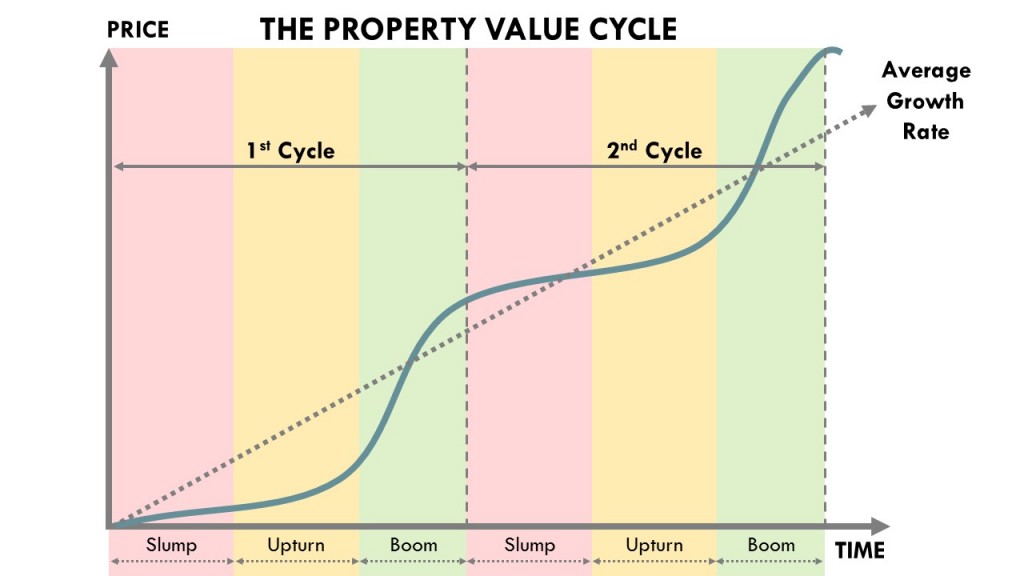

2. Property Value Cycle

Timing the market correctly can expedite your wealth creation, as property prices generally follow a 7 to 10 year cycle that is not linear. It is important to note that there are many property markets within Australia and each suburb has its own cycle.

Property cycles are not an exact science and past performance does not necessarily reflect future performance, so it is important to exercise caution and take the other factors into consideration when selecting an investment property.

As you can see in the chart above, most of the capital growth for a given market generally occurs in only 30% of the time for each cycle, which means that it is important to time the market correctly when purchasing an investment property. By identifying a potential property boom in advance and ideally purchasing at the end of the slump phase or in the early upturn phase, you can take advantage of the capital growth at the end of the boom phase and release the equity to purchase your next investment property without necessarily needing to use your cash.

Misjudging the market and buying a property at the end of a boom phase or in a hot market can significantly delay your capital gains and it may take several years before you realise any upside.

3. Education

Before purchasing your investment property, be sure to educate yourself and conduct thorough research.

You don’t need to be a property guru to be a successful property investor, however you should understand the fundamentals of property investment before you take the plunge to ensure that you are making an informed decision that has a high probability of achieving your financial objectives.

If you feel overwhelmed and need help, consider engaging a reputable and trustworthy property strategist to assist you. A word of caution here – there are lots of unscrupulous property spruikers out there, so be careful and ensure that you conduct the necessary due diligence before you part with your hard earned money.

4. Demographics

It is important to understand the demographics in each particular area you are researching before purchasing your investment property. Targeting the wrong demographic may negatively affect your investment returns and you may not achieve your objectives. Below are typical demographics to consider when selecting your investment property:

People

- Older couples and families

- Established coupes and families

- Maturing and established independence

- Maturing couples and families

- Elderly singles

- Older independence

- Independent youth

- Elderly couples

- Elderly families

- Young families

Employment Status

- Professionals

- Students

- Retirees

Wealth

- Household income

5. Dwelling Types

Investment returns can be impacted by dwelling types. For example, detached houses generally out-perform the other dwelling types when it comes to capital growth due to their land size, flexibility and desirability.

Be careful when investing in apartments as they generally don’t perform as well from a capital growth perspective and can be subject to over-supply, which can drive down prices and rental yields.

It is also important not to overcapitalise on your investment if you are building an investment property and land yourself in negative equity territory. It is easy to get carried away and select excessively high-end fixtures and fittings, however be careful not to go overboard and end up with a property that is worth less that what you paid for it. Remember – a property is only worth as much as someone is willing to pay for it!

Dwelling types typically include:

- Detached Houses

- Townhouses

- Duplexes

- Dual Occupancy

- Units

- Apartments

6. Rental Yield vs. Capital Growth

Property investors often focus too much on cash-flow and not enough on capital growth and their rate of wealth creation can be hampered as a result.

Whilst rental yield is important (it assists with cash-flow management and helps prevent negative gearing), many properties with high rental yields perform poorly when it comes to capital growth.

Passive income is important and wherever possible, your investment property should be cash-flow positive. However you should also aim to purchase a property which will return strong capital growth, as this approach will lead to maximised wealth in the long term.

What is rental yield?

Gross rental yield is the amount of gross rental income received per annum as a percentage of the current value of the property.

Gross Rental Yield (%) = (Total Annual Rental Income / Current Market Value) x 100

Example:

Joe owns an investment property, which he rents out for $600 per week and the property is currently valued at $650,000.

Therefore, the gross rental yield can be calculated as follows:

Annual rental income = $600 x 52 = $31,200

Gross Rental Yield = ($31,200 / $650,000) x 100 = 4.8%

What is capital growth?

Capital growth is the amount that a property increases in value over time and is calculated as follows:

Capital Growth (%) = (Change in Property Value / Original Value) x 100

Example:

Joe owns an investment property, which he purchased for $650,000. After one year of ownership, Joe’s bank re-valued his property at $700,000.

Therefore, the capital growth after one year can be calculated as follows:

Capital Growth (%) = (700,000 – $650,000) / $650,000

= ($50,000 / $650,000) x 100 = 7.7%

7. Pay the Right Price

Purchasing an investment property should not be an emotional decision. Be sure to run your numbers to ensure that you are buying the right property for the right price.

Avoid looking for a ‘cheap’ property that may remain ‘cheap’ in the long term and may not be attractive to potential future buyers.

Wherever possible, aim to negotiate a purchase price below the intrinsic value of the property to tap into early equity gains and accelerate your wealth creation.

8. Be Patient

Unlike some investment strategies, property investment is a long term wealth creation approach and is not a get rich quick scheme.

It is therefore important to be patient and not sell your investment property too soon just because it hasn’t gone up in value as quickly as you were hoping for. Many investors fall into the trap of selling too soon because they haven’t seen any capital growth and lose money just in time for the investor who bought their property to reap the rewards when the next boom comes along.

As Warren Buffet once said: “Successful investing takes time, discipline and patience. No matter how great the talent or effort, some things just take time: You can’t produce a baby in one month by getting nine women pregnant.”

Are you looking for an expert builder to help you grow your wealth and property portfolio?

Whether you are planning on building one or more properties or renovating an existing property, the friendly and experienced team at ARCA are here to help.

Call us for your obligation free consultation today on 1800 GENTRIFY or email us at enquiries@gentrify.com.au.

Disclaimer: The contents and information contained in this article are intended for general purposes only and should not be relied upon by any person as being complete or accurate. ARCA Pty Ltd, its employees, agents and other representatives will not accept any liability suffered or incurred by any person arising out of or in connection with any reliance on the content or of information contained in this article. This limitation applies to loss or damage of any kind, including but not limited to, compensatory, direct, indirect or consequential damage, loss of income or profit, loss of or damage to property and claims by any third party.